This data was collected from the LaGuardia Airport station in New York City for October 2018. It contains: - the daily minimum temperature (TMIN) - the daily maximum temperature (TMAX) - the daily average temperature (TAVG)

Note: The NCEI is part of the National Oceanic and Atmospheric Administration (NOAA) and, as you can see from the URL for the API, this resource was created when the NCEI was called the NCDC. Should the URL for this resource change in the future, you can search for “NCEI weather API” to find the updated one.

In addition, we will be using S&P 500 stock market data (obtained using the stock_analysis package and data for bitcoin for 2017 through 2018. For the first edition, the bitcoin data was collected from CoinMarketCap using the stock_analysis package; however, changes in the website led to the necessity of changing the data source to Yahoo! Finance. The bitcoin data that was collected before the CoinMarketCap website change should be equivalent to the historical data that can be viewed on this page.

Setup

We need to import pandas and read in the temperature data to get started:

import pandas as pddf = pd.read_csv('../data/nyc_temperatures.csv')df.head()

We want to rename the value column to indicate it contains the temperature in Celsius and the attributes column to say flags since each value in the comma-delimited string is a different flag about the data collection. For this task, we use the rename() method and pass in a dictionary mapping the column names to their new names. We pass inplace=True to change our original dataframe instead of getting a new one back:

This also works with Series/DataFrame objects that have an index of type DatetimeIndex. Let’s read in the CSV again for this example and set the date column to be the index and stored as a datetime:

We can use tz_convert() to convert to another timezone from there. If we convert the Eastern datetimes to UTC, they will now be at 5 AM, since pandas will use the offsets to convert:

eastern.tz_convert('UTC').head()

datatype

station

attributes

value

date

2018-10-01 05:00:00+00:00

TAVG

GHCND:USW00014732

H,,S,

21.2

2018-10-01 05:00:00+00:00

TMAX

GHCND:USW00014732

,,W,2400

25.6

2018-10-01 05:00:00+00:00

TMIN

GHCND:USW00014732

,,W,2400

18.3

2018-10-02 05:00:00+00:00

TAVG

GHCND:USW00014732

H,,S,

22.7

2018-10-02 05:00:00+00:00

TMAX

GHCND:USW00014732

,,W,2400

26.1

We can change the period of the index as well. We could change the period to be monthly to make it easier to aggregate later.

The reason we have to add the parameter within tz_localize() to None for this, is because we’ll get a warning from pandas that our output class PeriodArray doesn’t have time zone information and we’ll lose it.

We can use the assign() method for working with multiple columns at once (or creating new ones). Since our date column has already been converted, we need to read in the data again:

date datetime64[ns]

datatype object

station object

flags object

temp_C float64

temp_F float64

dtype: object

The date column now has datetimes and the temp_F column was added:

new_df.head()

date

datatype

station

flags

temp_C

temp_F

0

2018-10-01

TAVG

GHCND:USW00014732

H,,S,

21.2

70.16

1

2018-10-01

TMAX

GHCND:USW00014732

,,W,2400

25.6

78.08

2

2018-10-01

TMIN

GHCND:USW00014732

,,W,2400

18.3

64.94

3

2018-10-02

TAVG

GHCND:USW00014732

H,,S,

22.7

72.86

4

2018-10-02

TMAX

GHCND:USW00014732

,,W,2400

26.1

78.98

We can also use astype() to perform conversions. Let’s create columns of the integer portion of the temperatures in Celsius and Fahrenheit. We will use lambda functions (first introduced in Chapter 2, Working with Pandas DataFrames), so that we can use the values being created in the temp_F column to calculate the temp_F_whole column. It is very common (and useful) to use lambda functions with assign():

Say we want to find the days that reached the hottest temperatures in the weather data; we can sort our values by the temp_C column with the largest on top to find this:

However, this isn’t perfect because we have some ties, and they aren’t sorted consistently. In the first tie between the 7th and the 10th, the earlier date comes first, but the opposite is true with the tie between the 4th and the 2nd. We can use other columns to break ties and specify how to sort each with ascending. Let’s break ties with the date column and show earlier dates before later ones:

Notice that the index was jumbled in the past 2 results. Here, our index only stores the row number in the original data, but we may not need to keep track of that information. In this case, we can pass in ignore_index=True to get a new index after sorting:

The sample() method will give us rows (or columns with axis=1) at random. We can provide a seed (random_state) to make this reproducible. The index after we do this is jumbled:

df.sample(5, random_state=0).index

Index([2, 30, 55, 16, 13], dtype='int64')

We can use sort_index() to order it again:

df.sample(5, random_state=0).sort_index().index

Index([2, 13, 16, 30, 55], dtype='int64')

The sort_index() method can also sort columns alphabetically:

df.sort_index(axis=1).head()

datatype

date

flags

station

temp_C

temp_C_whole

temp_F

temp_F_whole

0

TAVG

2018-10-01

H,,S,

GHCND:USW00014732

21.2

21

70.16

70

1

TMAX

2018-10-01

,,W,2400

GHCND:USW00014732

25.6

25

78.08

78

2

TMIN

2018-10-01

,,W,2400

GHCND:USW00014732

18.3

18

64.94

64

3

TAVG

2018-10-02

H,,S,

GHCND:USW00014732

22.7

22

72.86

72

4

TMAX

2018-10-02

,,W,2400

GHCND:USW00014732

26.1

26

78.98

78

This can make selection with loc easier for many columns:

Now that we have an index of type DatetimeIndex, we can do datetime slicing and indexing. As long as we provide a date format that pandas understands, we can grab the data. To select all of 2018, we simply use df.loc['2018'], for the fourth quarter of 2018 we can use df.loc['2018-Q4'], grabbing October is as simple as using df.loc['2018-10']; these can also be combined to build ranges. Let’s grab October 11, 2018 through October 12, 2018 (inclusive of both endpoints)—note that using loc[] is optional for ranges:

df['2018-10-11':'2018-10-12']

datatype

station

flags

temp_C

temp_C_whole

temp_F

temp_F_whole

date

2018-10-11

TAVG

GHCND:USW00014732

H,,S,

23.4

23

74.12

74

2018-10-11

TMAX

GHCND:USW00014732

,,W,2400

26.7

26

80.06

80

2018-10-11

TMIN

GHCND:USW00014732

,,W,2400

21.7

21

71.06

71

2018-10-12

TAVG

GHCND:USW00014732

H,,S,

18.3

18

64.94

64

2018-10-12

TMAX

GHCND:USW00014732

,,W,2400

22.2

22

71.96

71

2018-10-12

TMIN

GHCND:USW00014732

,,W,2400

12.2

12

53.96

53

We can also use reset_index() to get a fresh index and move our current index into a column for safe keeping. This is especially useful if we had data, such as the date, in the index that we don’t want to lose:

df['2018-10-11':'2018-10-12'].reset_index()

date

datatype

station

flags

temp_C

temp_C_whole

temp_F

temp_F_whole

0

2018-10-11

TAVG

GHCND:USW00014732

H,,S,

23.4

23

74.12

74

1

2018-10-11

TMAX

GHCND:USW00014732

,,W,2400

26.7

26

80.06

80

2

2018-10-11

TMIN

GHCND:USW00014732

,,W,2400

21.7

21

71.06

71

3

2018-10-12

TAVG

GHCND:USW00014732

H,,S,

18.3

18

64.94

64

4

2018-10-12

TMAX

GHCND:USW00014732

,,W,2400

22.2

22

71.96

71

5

2018-10-12

TMIN

GHCND:USW00014732

,,W,2400

12.2

12

53.96

53

Reindexing allows us to conform our axis to contain a given set of labels. Let’s turn to the S&P 500 stock data in the sp500.csv file to see an example of this. Notice we only have data for trading days (weekdays, excluding holidays):

If we want to look at the value of a portfolio (group of assets) that trade on different days, we need to handle the mismatch in the index. Bitcoin, for example, trades daily. If we sum up all the data we have for each day (aggregations will be covered in chapter 4, so don’t fixate on this part), we get the following:

bitcoin = pd.read_csv('../data/bitcoin.csv', index_col='date', parse_dates=True).drop(columns=['market_cap'])# every day's closing price = S&P 500 close + Bitcoin close (same for other metrics)portfolio = pd.concat([sp, bitcoin], sort=False).groupby(level='date').sum()portfolio.head(10).assign( day_of_week=lambda x: x.index.day_name())

high

low

open

close

volume

day_of_week

date

2017-01-01

1003.080000

958.700000

963.660000

998.330000

147775008

Sunday

2017-01-02

1031.390000

996.700000

998.620000

1021.750000

222184992

Monday

2017-01-03

3307.959883

3266.729883

3273.170068

3301.670078

3955698000

Tuesday

2017-01-04

3432.240068

3306.000098

3306.000098

3425.480000

4109835984

Wednesday

2017-01-05

3462.600000

3170.869951

3424.909932

3282.380000

4272019008

Thursday

2017-01-06

3328.910098

3148.000059

3285.379893

3179.179980

3691766000

Friday

2017-01-07

908.590000

823.560000

903.490000

908.590000

279550016

Saturday

2017-01-08

942.720000

887.250000

908.170000

911.200000

158715008

Sunday

2017-01-09

3189.179990

3148.709902

3186.830088

3171.729902

3359486992

Monday

2017-01-10

3194.140020

3166.330020

3172.159971

3176.579902

3754598000

Tuesday

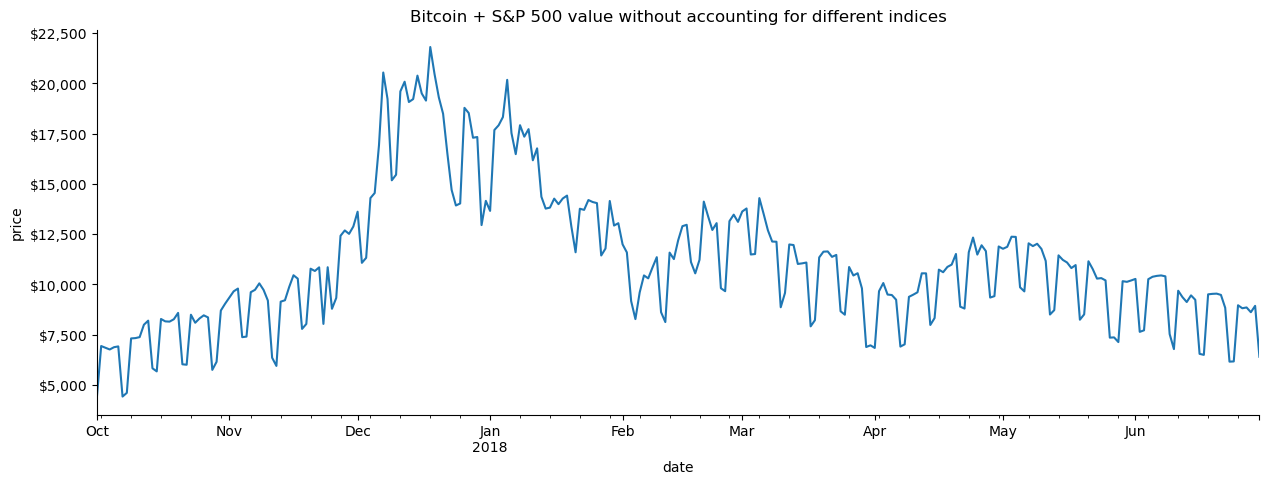

It may not be immediately obvious what is wrong with the previous data, but with a visualization we can easily see the cyclical pattern of drops on the days the stock market is closed. (Don’t worry about the plotting code too much, we will cover it in depth in chapters 5 and 6).

We will need to import matplotlib now:

import matplotlib.pyplot as plt # we use this module for plottingfrom matplotlib.ticker import StrMethodFormatter # for formatting the axis

Now we can see why we need to reindex:

# plot the closing price from Q4 2017 through Q2 2018ax = portfolio['2017-Q4':'2018-Q2'].plot( y='close', figsize=(15, 5), legend=False, title='Bitcoin + S&P 500 value without accounting for different indices')# formattingax.set_ylabel('price')ax.yaxis.set_major_formatter(StrMethodFormatter('${x:,.0f}'))for spine in ['top', 'right']: ax.spines[spine].set_visible(False)# show the plotplt.show()

We need to align the index of the S&P 500 to match bitcoin in order to fix this. We will use the reindex() method, but by default we get NaN for the values that we don’t have data for:

So now we have rows for every day of the year, but all the weekends and holidays have NaN values. To address this, we can specify how to handle missing values with the method argument. In this case, we want to forward-fill, which will put the weekend and holiday values as the value they had for the Friday (or end of trading week) before:

To isolate the changes happening with the forward-filling, we can use the compare() method. It shows us the values that differ across identically-labeled dataframes (same names and same columns). Here, we can see that only weekends and holidays (Monday, January 16, 2017 was MLK day) have values forward-filled. Notice that consecutive days have the same values.

This isn’t perfect though. We probably want 0 for the volume traded and to put the closing price for the open, high, low, and close on the days the market is closed:

The reason why we’re using np.where(boolean condition, value if True, value if False) within lambda functions in the example below, is that vectorized operations allow us to be faster and more efficient than utilizing for loops to perform calculations on arrays all at once.

import numpy as npsp_reindexed = sp.reindex(bitcoin.index).assign( volume=lambda x: x.volume.fillna(0), # put 0 when market is closed close=lambda x: x.close.fillna(method='ffill'), # carry this forward# take the closing price if these aren't availableopen=lambda x: np.where(x.open.isnull(), x.close, x.open), high=lambda x: np.where(x.high.isnull(), x.close, x.high), low=lambda x: np.where(x.low.isnull(), x.close, x.low))sp_reindexed.head(10).assign( day_of_week=lambda x: x.index.day_name())

high

low

open

close

volume

day_of_week

date

2017-01-01

NaN

NaN

NaN

NaN

0.000000e+00

Sunday

2017-01-02

NaN

NaN

NaN

NaN

0.000000e+00

Monday

2017-01-03

2263.879883

2245.129883

2251.570068

2257.830078

3.770530e+09

Tuesday

2017-01-04

2272.820068

2261.600098

2261.600098

2270.750000

3.764890e+09

Wednesday

2017-01-05

2271.500000

2260.449951

2268.179932

2269.000000

3.761820e+09

Thursday

2017-01-06

2282.100098

2264.060059

2271.139893

2276.979980

3.339890e+09

Friday

2017-01-07

2276.979980

2276.979980

2276.979980

2276.979980

0.000000e+00

Saturday

2017-01-08

2276.979980

2276.979980

2276.979980

2276.979980

0.000000e+00

Sunday

2017-01-09

2275.489990

2268.899902

2273.590088

2268.899902

3.217610e+09

Monday

2017-01-10

2279.270020

2265.270020

2269.719971

2268.899902

3.638790e+09

Tuesday

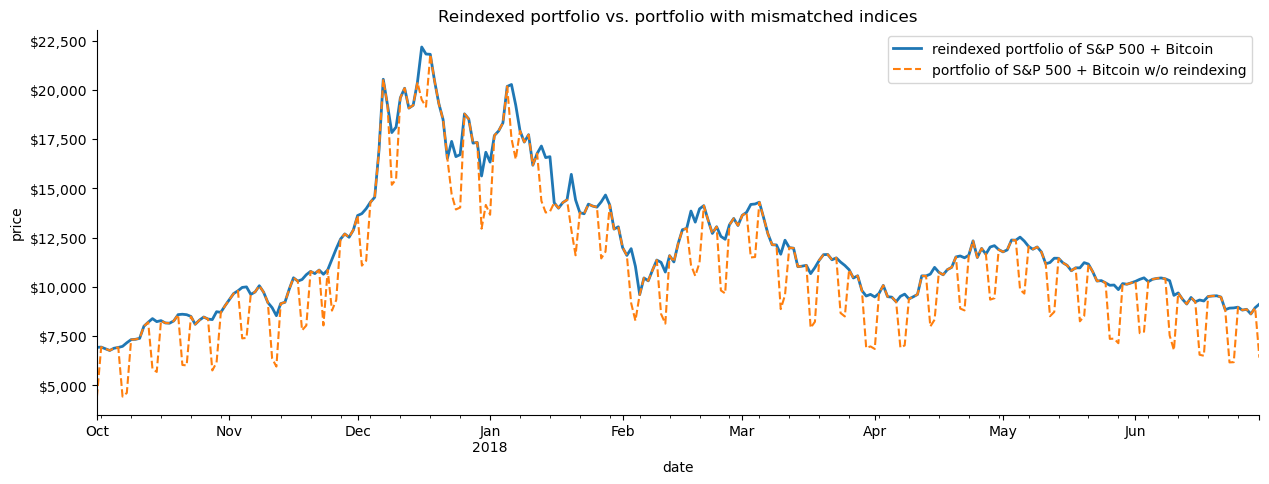

If we create a visualization comparing the reindexed data to the first attempt, we see how reindexing helped maintain the asset value when the market was closed:

# every day's closing price = S&P 500 close adjusted for market closure + Bitcoin close (same for other metrics)fixed_portfolio = sp_reindexed + bitcoin# plot the reindexed portfolio's closing price from Q4 2017 through Q2 2018ax = fixed_portfolio['2017-Q4':'2018-Q2'].plot( y='close', label='reindexed portfolio of S&P 500 + Bitcoin', figsize=(15, 5), linewidth=2, title='Reindexed portfolio vs. portfolio with mismatched indices')# add line for original portfolio for comparisonportfolio['2017-Q4':'2018-Q2'].plot( y='close', ax=ax, linestyle='--', label='portfolio of S&P 500 + Bitcoin w/o reindexing')# formattingax.set_ylabel('price')ax.yaxis.set_major_formatter(StrMethodFormatter('${x:,.0f}'))for spine in ['top', 'right']: ax.spines[spine].set_visible(False)# show the plotplt.show()